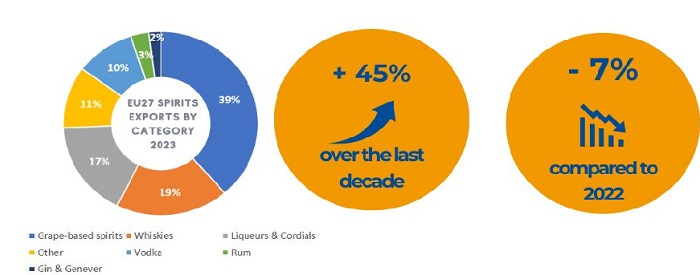

The EU spirits sector has demonstrated resilience in 2023, surpassing the value of €9.07 billion in global exports in the face of a challenging year, marked by continued geopolitical tensions and significant inflation. This is largely thanks to a good performance in Asia, which has offset a more challenging year in other markets, not least the US. Overall, the figure for 2023 marks a decrease of EU spirits exports in value of 7% compared with 2022, which was a particularly strong year, due to the reopening of borders, tourism and the hospitality sector in most markets. As in previous years, the biggest category in value was grape & marc-based spirits, representing 39% of our total exports, followed by whiskies (19%), liqueurs & cordials (17%), spirituous beverages & other categories (11%) and vodka (10%).

It is worth stressing that the value of EU spirits exports in 2023 remains above 2021 and pre-pandemic levels, despite a challenging year, putting this decline into perspective. That said, the overall growth of the value of EU spirits exports over the last decade seems to be slowing down (from a 65% growth rate between 2011 and 2021, to a 45% growth rate between 2013 and 2023). This is a reminder that our export success story cannot be taken for granted. It stresses the need for continued support from trade and promotion policies to open new markets and opportunities, with a focus on high-potential markets, while maintaining growth in more established markets. This is needed to reinforce and secure the sustainable growth of EU spirits’ exports, with a strong focus on premiumisation and on geographical indications, which represent around 2/3 of EU spirits exports in value.

When looking at the list of top 3 export markets for EU spirits, while the ranking itself has not changed, the figures provide a very contrasted picture of the situation. The US market remains the first export destination in value by far for EU spirits, with exports worth €2.76 billion, but has seen a decline of 27% of exports in value compared with 2022. This is partly due to the reduction of overstocks built after the pandemic, and to a combination of more challenging global economic conditions and rising living costs for consumers in the US. However, the end of 2023 shows some encouraging signs of recovery. It will be critical to support this recovery by ensuring that the tariffs that were imposed on EU spirits in the frame of the large civil aircrafts disputes and that are suspended until mid-2026 do not return. The same goes for tariffs imposed on US spirits in the frame of the steel & aluminium dispute (suspended until March 2025) and large civil aircrafts disputes, which would have a detrimental impact on EU producers invested in the US and on US producers with investment in the EU, and in turn on their ability to keep investing in EU categories. Resolving these disputes and ensuring that unrelated sectors are not hit by a return of tariffs is therefore critical.

In contrast, China and the UK performed better, with exports in value of €889 million and €852 million respectively, and with positive, albeit subdued, growth in value in both markets (+2% and +8% respectively), demonstrating their continued importance for our sector.

When turning to high-potential markets, the picture is quite contrasted, with a positive performance in India (+7%) and in ASEAN countries (+10% in value overall) – particularly in Malaysia (+9%), Thailand (+35%) and Indonesia (+105%), and a less positive performance in Sub-Saharan Africa and Latin America (-7% and -13% respectively).

Looking at India and ASEAN: while most of these markets still represent a relatively modest share of overall EU spirits exports in value, their potential is clear. It only reinforces the importance of trade negotiations with these countries, starting with India, where our products face an import duty of 150%. The same is true for ongoing negotiations with Thailand and Indonesia, where EU spirits currently face import duties of up to 60% and 150% respectively. Efforts should also focus on Malaysia, where EU spirits are at an increasing disadvantage compared with spirits producers from CPTPP members, and on the Philippines, which remain a key export destination for EU spirits with exports still worth €167 million in 2023 in spite of a year-on year decrease of 19% in value.

Last but certainly not least, it is high time the EU-Mercosur FTA were ratified, to eliminate tariffs on EU spirits, increase the protection of geographical indications and help address non-tariff barriers. Such a boost is urgent, after what has been a particularly challenging year for EU spirits in the Mercosur region (-47% in value in Argentina, -26% in Brazil and -24% in Uruguay).

As we are approaching the end of the current European Commission mandate and the start of a new one, it is time to reflect on the results of trade policy in the last years and what is needed to support exporters in the second half of the decade. While we have seen a strong focus on sustainability, security and on defensive trade instruments in the last years, we regret the more modest progress in the FTAs agenda. While we have a good network of existing FTA partners, we must avoid becoming complacent. With 85% of global growth expected to take place outside of the EU in the coming years and key markets still being out of the existing EU FTAs network (particularly India, Mercosur & most ASEAN members), opening up new markets and providing the means for companies to diversify will be essential for most economic sectors in the EU. This is of course particularly the case for exports-driven sectors such as ours, who depend on a strong export performance to support rural areas, growth and jobs in the EU. We trust that this will be front and centre in all policymakers’ minds as attention starts turning to what will come after June 2024.